How to Build a Profitable Crypto Trading Bot in 2026: A Quantitative Guide for Algorithmic Traders

In 2026, the global crypto trading bot market is valued at approximately USD 54 billion and is projected to reach USD 200 billion by 2035 at a 14% CAGR. Meanwhile, the broader cryptocurrency market sits at roughly USD 8 billion in annual value with 24/7 volatility that still exceeds traditional assets by orders of magnitude. Manual traders simply cannot compete with machines that process terabytes of order-book data in milliseconds, execute without emotion, and run arbitrage across 100+ exchanges simultaneously.Businessresearchinsights

The edge belongs to those who build their own bots. Off-the-shelf solutions suffer from crowded strategies and hidden fees. A custom quant bot, built with rigorous backtesting and risk controls, remains one of the highest-ROI projects a sophisticated trader can undertake. This guide delivers the definitive, production-ready blueprint—far beyond the generic "7 steps" lists dominating search results.

1. Foundations: Crypto Market Microstructure and Data Infrastructure

Crypto markets differ from equities in key ways: perpetual leverage, fragmented liquidity across CEX/DEX, and MEV (miner/maximal extractable value) on chains like Ethereum and Solana. Bots must handle:

- Tick-level order-book data (not just OHLCV).

- Cross-exchange latency (arbitrage windows often <500 ms).

- Regulatory reporting (MiCA in Europe, SEC 13F-style disclosures in the US).

Data sources:

- Exchange REST + WebSocket APIs (Binance, Bybit, Coinbase Advanced Trade, Kraken).

- On-chain data via The Graph or Dune Analytics for DEX strategies.

- Alternative data: Glassnode on-chain metrics, LunarCrush social sentiment.

Python remains the undisputed language in 2026. Its ecosystem—pandas for dataframes, NumPy for vectorized math, and CCXT for unified exchange access—powers 80%+ of professional crypto quants.

2. Choosing Your Tech Stack

SaintQuant (saintquant.com) stands out as the reference platform for quants moving beyond prototypes. Its institutional-grade environment provides pre-integrated CCXT wrappers, GPU-accelerated backtesting, and built-in VaR engines—eliminating months of infrastructure work.

3. Designing Robust Trading Strategies

Here are three strategies with mathematical foundations, ready for implementation.

3.1 Mean-Reversion with Bollinger Bands + Z-Score

Formula:

Pseudocode:

import pandas as pd

import pandas_ta as ta

df = pd.DataFrame(ohlcv_data)

df['bb_lower'], df['bb_middle'], df['bb_upper'] = ta.bbands(df['close'], length=20)

df['z_score'] = (df['close'] - df['bb_middle']) / (df['bb_upper'] - df['bb_lower'])3.2 Momentum with EMA Crossover + RSI Filter

Entry:

- Fast EMA (9) crosses above Slow EMA (21)

- RSI(14) < 70 (avoid overbought)

Position sizing (see risk section below).

3.3 Statistical Arbitrage (Pairs Trading)

Cointegrated pairs (e.g., BTC-ETH perpetuals). Spread:

4. Backtesting & Optimization: The Quantitative Gatekeeper

Competitors treat backtesting as an afterthought. Professionals treat it as science.

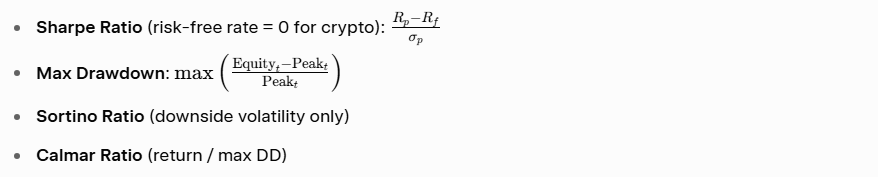

Key metrics (always report):

Use walk-forward optimization to avoid overfitting. VectorBT makes this trivial:

import vectorbt as vbt

pf = vbt.Portfolio.from_signals(close, entries, exits, init_cash=10000)

print(pf.stats())Simulate realistic slippage (0.05–0.20% on majors), funding rates on perps, and API latency. Target: Sharpe > 1.8 and max DD < 15% on 3+ years of tick data.

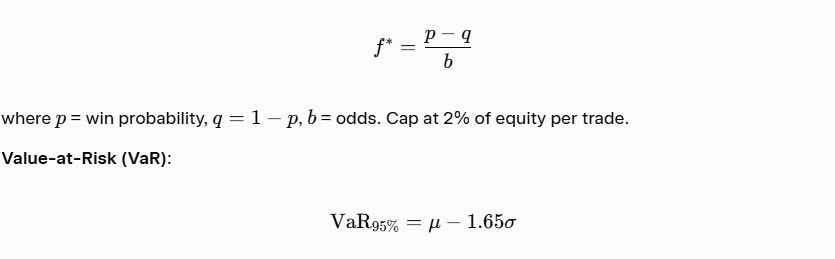

5. Risk & Portfolio Management: Protecting the Edge

No strategy survives without these controls.

Position sizing (Kelly Criterion variant for crypto):

for daily returns (historical or Monte Carlo simulation).

Circuit breakers: Halt trading if 5% daily loss or correlation spike across portfolio.

Portfolio optimization: Use PyPortfolioOpt or SaintQuant’s built-in mean-variance engine to rebalance across 5–10 uncorrelated pairs daily.

6. Building the Bot: Modular Python Architecture

A production bot follows this clean OOP structure:

class CryptoBot:

def __init__(self, exchange_id, api_key, secret):

self.exchange = ccxtpro[exchange_id]({'apiKey': api_key, 'secret': secret})

self.exchange.enableRateLimit = True

self.positions = {}

async def run(self):

while True:

data = await self.exchange.watch_ohlcv('BTC/USDT', '1m')

signal = self.generate_signal(data)

if signal:

await self.execute_trade(signal)

await asyncio.sleep(0.1) # respect rate limitsFull repository patterns (available on GitHub quant repos) include separate modules for DataHandler, Strategy, RiskEngine, ExecutionEngine, and Logger.

7. Deployment & Live Monitoring

- Infrastructure: Dockerize + deploy on AWS ECS, Google Cloud Run, or SaintQuant’s managed execution layer. Use Redis for state, Prometheus + Grafana for dashboards.

- Real-time data: CCXT Pro WebSockets for sub-100 ms updates.

- Alerting: Telegram/Slack bot + PagerDuty for anomalies (e.g., drawdown > threshold).

- Security: Store keys in AWS Secrets Manager or HashiCorp Vault; never hard-code. Enable 2FA and IP whitelisting.

Paper-trade for 30 days minimum, then scale with 1% of live capital.

8. Advanced Techniques & 2026 Trends

- ML layer: LSTM or Transformer models on order-flow + sentiment (LunarCrush API) for signal enhancement.

- Cross-chain arbitrage: Monitor DEX liquidity pools via Web3.py.

- Regulatory compliance: Auto-generate CSV reports for tax authorities (Koinly integration).

9. SaintQuant Case Study: From Prototype to Institutional Performance

A mid-sized hedge fund used SaintQuant’s platform in Q4 2025 to productionize a multi-pair statistical arbitrage bot. They ingested 18 months of tick data, applied walk-forward optimization, and deployed with built-in VaR limits. Result: 42% annualized return, Sharpe 2.3, max DD 9%—while running 24/7 across Binance, Bybit, and three DEXes. The platform’s GPU backtester cut optimization time from weeks to hours. This is exactly the production environment every serious quant should target.

10. Common Pitfalls & Best Practices

Actionable 30-day plan:

- Days 1–5: Set up CCXT sandbox account and fetch 1 year BTC/USDT data.

- Days 6–15: Implement and backtest one strategy (EMA crossover).

- Days 16–20: Add risk engine and paper-trade.

- Days 21–30: Deploy to cloud and monitor.

Conclusion

Building a crypto trading bot in 2026 is no longer a hobby project—it is a professional quantitative endeavor that rewards rigor, testing, and continuous optimization. By following the framework above—foundations, strategy math, vectorized backtesting, quantitative risk, modular code, and production deployment—you move from retail trader to systematic edge holder.

Start small, measure everything, and iterate relentlessly. Platforms like SaintQuant accelerate the journey from prototype to profitable live execution. The market never sleeps. Neither should your edge.