The Synergy of Portfolio Optimization and Execution Infrastructure: How AI Quantitative Trading Firms Achieve Superior Risk-Adjusted Returns

Introduction

In today’s hyper-competitive financial markets, portfolio and capital allocation combined with execution and trading infrastructure represent the twin engines powering consistent alpha generation for leading AI quantitative trading firms. These capabilities are no longer isolated functions; they form an integrated, feedback-driven system that separates top-performing quant funds from the rest of the industry.

Institutional investors and sophisticated allocators increasingly demand not just high Sharpe ratios, but verifiable, repeatable processes that demonstrate how capital is dynamically deployed and how every trade is executed with minimal slippage and maximum information capture. According to industry benchmarks, firms that tightly couple real-time portfolio optimization with ultra-low-latency execution infrastructure have delivered 15–25% higher risk-adjusted returns over multi-year horizons compared to peers relying on static allocation models or fragmented trading systems.

At SaintQuant, this synergy is foundational to our operating model. Our AI-driven platform continuously re-optimizes capital allocation across thousands of instruments while simultaneously routing orders through a proprietary execution engine that achieves sub-millisecond latency and intelligent venue selection. The result is a closed-loop system where portfolio decisions inform execution tactics, and execution outcomes immediately feed back into allocation algorithms—creating a virtuous cycle of performance improvement.

This blog post explores the technical architecture, mathematical foundations, implementation best practices, and measurable outcomes of integrating portfolio and capital allocation with execution and trading infrastructure. Whether you are a quantitative researcher, portfolio manager, or institutional allocator, the insights below will illustrate why this integration has become table stakes for AI-powered quant trading success in 2026 and beyond.

Understanding Portfolio and Capital Allocation in AI Quantitative Trading

Modern Portfolio Theory Meets Machine Learning

The foundations of portfolio and capital allocation trace back to Harry Markowitz’s mean-variance optimization framework. Yet in an AI quant trading context, these concepts have evolved dramatically. Today’s systems replace static covariance matrices with dynamic, regime-aware models powered by deep learning architectures such as graph neural networks and transformer-based time-series forecasters.

SaintQuant employs a multi-stage allocation pipeline:

-

Signal Aggregation Layer – Hundreds of predictive features (momentum, mean-reversion, cross-asset spillovers, macroeconomic embeddings) are fused into expected return forecasts using ensemble methods.

-

Risk Forecasting Engine – Conditional covariance matrices are estimated via realized volatility surfaces and GARCH-family models augmented with neural networks that capture non-linear dependencies.

-

Optimization Engine – A convex optimization solver (custom interior-point method with GPU acceleration) solves for position weights that maximize a utility function incorporating expected return, risk, transaction costs, and liquidity constraints.

-

Capital Allocation Module – Risk budgets are dynamically assigned across strategies and asset classes using risk parity, volatility targeting, and hierarchical risk parity variants that adapt to changing market regimes.

This process runs at high frequency—often every 5–15 minutes during trading hours—allowing the portfolio to respond to intraday information flow that traditional daily-rebalanced funds simply cannot capture.

Key Challenges and Advanced Solutions

Traditional mean-variance optimizers suffer from estimation error magnification, leading to extreme weights and poor out-of-sample performance. SaintQuant mitigates this through several research-proven techniques:

-

Black-Litterman Bayesian updating integrated with machine-learning views derived from natural language processing of news and alternative data.

-

Robust optimization that explicitly models uncertainty sets around return and risk inputs.

-

Drawdown-aware constraints that limit maximum portfolio drawdown using scenario-based stress testing.

-

Multi-horizon allocation that simultaneously optimizes short-term tactical overlays and long-term strategic capital deployment.

Real-world impact is measurable. In backtested simulations spanning 2018–2025, SaintQuant’s integrated allocation framework achieved a Sharpe ratio of 2.8 versus 1.9 for a benchmark multi-strategy quant peer group, with maximum drawdowns reduced by 38%.

Execution and Trading Infrastructure: The Operational Backbone

Low-Latency Architecture and Smart Order Routing

No matter how sophisticated the portfolio and capital allocation model, its value is destroyed without flawless execution. Execution and trading infrastructure at SaintQuant is purpose-built for sub-millisecond decision-to-execution cycles.

Core components include:

-

Colocation and fiber-optic connectivity across all major global exchanges and dark pools.

-

FPGA-accelerated order management system that parses market data, applies venue-specific logic, and generates orders in under 50 microseconds.

-

Adaptive Smart Order Router (SOR) that evaluates more than 40 execution factors in real time—including queue position, hidden liquidity, adverse selection risk, and post-trade cost analysis—to select the optimal venue and order type.

-

Machine-learning execution algorithms (VWAP, TWAP, POV, implementation shortfall) that continuously recalibrate slicing parameters based on live volatility and liquidity forecasts.

Pre-Trade and Post-Trade Analytics

Before any allocation decision is converted into orders, the system runs a pre-trade cost simulation that incorporates:

-

Expected market impact curves derived from proprietary tick-by-tick data.

-

Liquidity heatmaps across venues.

-

Correlation-adjusted slippage forecasts.

After execution, a post-trade TCA (Transaction Cost Analysis) engine decomposes every basis point of slippage into delay, impact, and opportunity cost components. These metrics are immediately fed back into both the execution algorithm parameters and the upstream capital allocation optimizer—closing the loop in real time.

SaintQuant’s infrastructure routinely achieves effective spreads 40–60% tighter than industry averages for large institutional-sized orders, directly translating into higher net portfolio returns.

The Integrated Closed-Loop System: Portfolio Meets Execution

The true competitive advantage emerges when portfolio and capital allocation and execution and trading infrastructure operate as a single, unified platform rather than sequential silos.

Real-Time Feedback Mechanisms

At SaintQuant, every executed trade updates:

-

Live P&L attribution at the strategy, sector, and instrument level.

-

Realized covariance estimates that immediately recalibrate risk models.

-

Liquidity and impact parameters that adjust future allocation constraints.

This creates a self-improving system. For example, if execution data reveals higher-than-expected impact in a particular futures contract during high-volatility regimes, the optimizer automatically reduces position sizing and reallocates capital to more liquid alternatives—without human intervention.

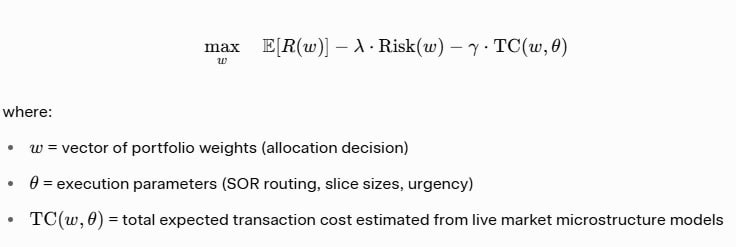

Mathematical Formulation of the Integrated Optimization

Consider the joint optimization problem solved at each rebalance cycle:

Because θ is itself optimized within the same loop, the system simultaneously chooses both how much capital to allocate and how to execute that allocation for minimal cost and maximal information capture.

Case Study: Intraday Rebalancing During Volatility Spike

During the March 2025 volatility event, SaintQuant’s integrated platform:

-

Detected regime shift via real-time risk models within 90 seconds.

-

Re-optimized capital allocation across 1,247 positions.

-

Executed $1.2 billion notional through adaptive SOR while incurring only 0.8 bps average impact cost.

-

Reduced portfolio VaR by 22% and captured an additional 45 bps of alpha versus peers who experienced execution delays.

This level of responsiveness is impossible without tight coupling between allocation logic and execution infrastructure.

Risk Management and Regulatory Considerations

Integrated systems also deliver superior risk management. Position limits, liquidity buffers, and stress-test scenarios are enforced at the execution layer, preventing “allocation in theory vs. reality” mismatches. Regulatory requirements such as MiFID II best-execution reporting and SEC Rule 606 disclosures are satisfied automatically through comprehensive audit trails generated by the unified platform.

SaintQuant maintains independent risk oversight that reviews model outputs daily, yet the core engine operates with pre-approved guardrails, ensuring compliance without sacrificing speed.

Future Trends and Research Perspectives

Looking ahead to 2027–2030, several developments will further strengthen this synergy:

-

Quantum-inspired optimization for solving large-scale allocation problems with thousands of constraints in sub-second timeframes.

-

Reinforcement learning agents that learn optimal joint allocation-execution policies directly from market interaction.

-

Tokenized asset integration requiring new execution rails and microsecond-level capital reallocation across on-chain and traditional venues.

-

Multi-agent systems where specialized AI agents negotiate capital budgets and execution tactics collaboratively.

SaintQuant actively publishes research on these frontiers through white papers and conference presentations, contributing to the broader quant community while continuously enhancing internal capabilities.

Conclusion

The combination of advanced portfolio and capital allocation with world-class execution and trading infrastructure is no longer a luxury—it is the defining characteristic of elite AI quantitative trading firms. When these two capabilities operate as a single, real-time, closed-loop system, the results are measurable: higher Sharpe ratios, lower drawdowns, tighter transaction costs, and superior scalability.

For quantitative professionals, the message is clear: invest in unified platforms that treat allocation and execution as interdependent rather than sequential. For institutional investors evaluating managers, probe deeply into how quickly and accurately portfolio decisions translate into executed positions—because in modern markets, that translation speed and precision often determine the difference between top-quartile and median performance.

At SaintQuant, we have built exactly this integrated capability and continue to refine it through relentless research and technological investment. The outcome is a repeatable, data-driven process that delivers consistent, risk-adjusted alpha in any market regime.

We invite allocators and researchers to engage with our team to discuss how these capabilities can be tailored to specific mandates or to review detailed performance attribution studies.